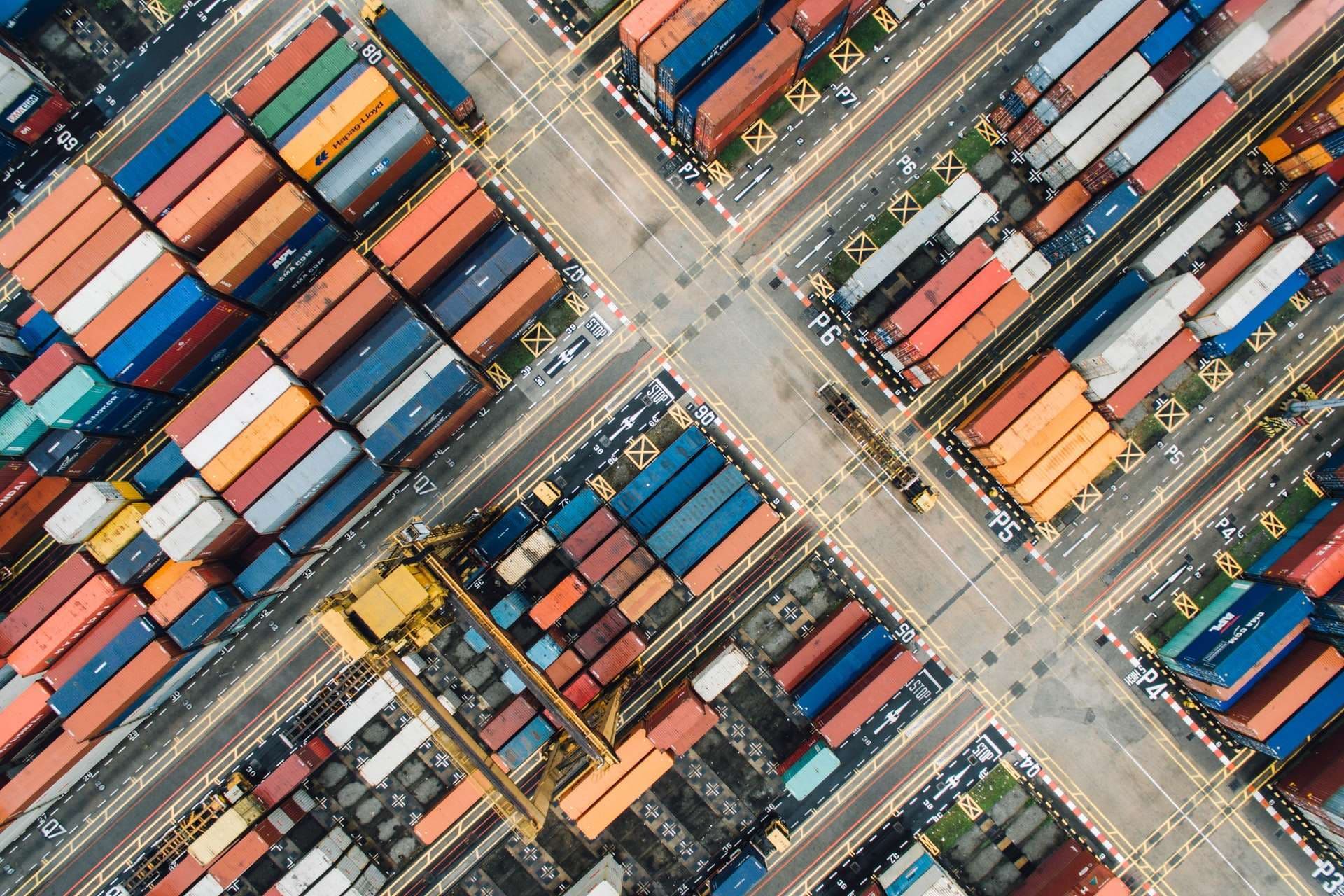

The Container Supply Crisis and the Changing World of Freight Logistics

For over thirty years now I have been fortunate enough to work in the world of logistics, first in the shipping sector and then in the ports sector. It has been a fascinating ride, and there have been familiar cyclical patterns combined with the occasional black swan event. I cannot recollect however any event where the entire freight and transportation sector got it so universally wrong as in the immediate forecasts for the freight transportation sector when COVID emerged in January 2020. One of the consequences of this is that the world has, to put it simply, run out of containers. It is this phenomenon of container shortage that is the subject of this brief paper.

For the first time the possession of a container asset has become a critical weapon in the competition for freight. Whole industry segments find their access to boxes disappearing, typically because they have the misfortune to be low rated or simply to be moving between geographies inconvenient to container fleet management. For example, moving animal feed from Europe to the Middle East using surplus European boxes pre-covid was relatively easy; happy to find a back-load to reposition otherwise empty containers to export dominant China, it was no great inconvenience to make a wayport call at Dubai on the way. The box fleet of carriers had enough slack for the extra week’s deviation. Today the carriers are focused on getting those empties back to China as empties because it is quicker, the fleet size is tight and the export freight rates from China are at unprecedented heights, hundreds of percent above the low points in the cycle. Just get that box back to China quickly! The same goes for other commodities: recycled materials, logs, pulp, plastics. Anyone moving their personal possessions as part of an overseas relocation during this time and requiring a 40’ container would also receive a nasty shock on their invoice!

So how did we get to this place?

To start with the narrative, when COVID emerged businesses in all sectors acted with prudence, protecting cash and balance sheets. Capital expenditure was halted, staff were furloughed as the world prepared for factories to close and freight to reduce to a trickle. Demand for goods would reduce. Except that is not what happened. Rather after a 6 week close down Chinese factories re-opened. Consumer demand in the USA and Europe boomed. There was a lag of course in this linear progression, but by July 2020 the pattern was clear. One of the consequences of working from home in the West, it transpired, was that many of us went on a spending spree facilitated by e-commerce shopping platforms, and a consumer spending power frustrated in its attempts to spend on services and entertainment that required mobility instead decided to spend on the home and hearth.

And what a spending spree it was! 2021 is now recognized as the largest re-stocking event in American history.

The crisis becomes self-perpetuating also. 30 ships at anchor outside Californian ports the norm, congested terminals in the main north European port range requiring days at anchor. Congestion reduces box availability in its own right as more boxes are needed to feed the same supply chain as parts of the chain grind to a walking or waiting pace. Pockets of stranded containers in import dominant surplus parts of the world also accumulate after tipping as the carriers cannot afford to wait on the berth and evacuate them all.

At the heart of this shortage also lay what happened in the container factories in the period from March to June 2020. First production reduced and then the factories closed altogether, as the forecasted demand collapse ended the need for containers. This as it turns out was critical. In any one year approximately 3.5-4 million TEU of new container builds are injected into the world fleet; shutting down for a quarter therefore deprives the freight industry of approximately 1 million TEU. That made supply side recovery impossible. The planned total close down for June to August was reversed in July, but too late.

In this modern world of systems and KPIs was this not preventable? I think it would be tough to prevent with the current industry dynamics. To start at its most basic, there is no-one who can advise accurately how many containers exist in the world. This question is a bit like asking how many cars are there in the world. Neither container buyers nor car buyers are kept on a global registry by any authority, and then there is the tricky question of how long these assets are kept in service, kept roadworthy so to speak. There are of course multiple container fleet operators across the carrier and leasing sectors. Based on a press release when Triton containers and TAL International merged in 2015 the merger created a combined fleet of 4.8 million TEU, a combined share of 25% of the leasing market. Putting this together with various estimates from maritime consultants such as Drewry Maritime reserch, we come to a modern fleet capacity in the order of some 70-75 million TEU, of which an estimated one-third are ex-service containers beyond the 12–14 year normal lifespan. So shutting down the factories for a quarter and losing 1 million TEU effectively took out 2% from the normally in-service fleet. On top of the largest re-stocking event in American history – that will do it I think.

Of course, this also needs to be understood in the wider context of supply and demand. Today the global shipping fleet is effectively fully utilized and scrapping rates are at their lowest level for years. So there is a wider narrative of tight supply of services and wider challenges; this was not going to be an easy period even if box supply was abundant. It is interesting to note however that those who can provide their own box have been offered more competitive rates or greater space opportunity on certain routes, so the container issue is very much in the issue mix.

So where do we go from here?

To my mind, the world of freight logistics must do better than this and the shortage has demonstrated that a fundamental business model that has existed since the birth of containerisation in the sixties is now ripe to be challenged. What we have now is insufficiently flexible and robust.

When the customer books cargo with a shipping line he gets two things: guaranteed space on a ship and a box to put his cargo in. Why do these two always come twinned? If there was a far larger box leasing segment that stood alongside the carrier fleets and the leasing company fleets (who lease to carriers), then there would have been a safety net of Shipper Owned Containers (SOCs).

The point could be made that SOCs exist today. They do, but the numbers are small and their usage has become marginalized because it is often seen by freight practitioners as simply too hard and time consuming to fit into the container industry machine that has become conditioned to producing large loads for large industrial enterprises. Back in February Lloyd’s List reported ContainerxChange conducting a “mystery shopper” survey of fifty top forwarders using a fake company ordering a shipment of coffee machine parts from China to Germany, specifying the use of a shipper owned container. Twelve of the forwarders accepted the booking, but only five could organize SOC transport and source a container. It indicated a lack of familiarity and interest. This reminds me a little of when I first started working for a container carrier in the 1980s, where the carrier had a small department which still specialised in conventional Out of Gauge cargo, full of experienced cargo professionals who could calculate and pack cargo using skills that were marginalised by the established new orthodoxy of “box plus space”: they had a different outlook on a standard process.

To grow this third party box sector however requires some new frameworks, and this is something that the Digital Freight Alliance (DFA) is looking at today. The DFA is a Membership Association founded in 2020, which puts freight forwarders in touch with each other, in a mutually supportive network and provides payment protection for its members who do business with each other through a series of booking platforms and digital tools provided. We are working to a position where we can say to members on selected routes “do you want a container with that?”.

For this to work however there are a couple of realities which need to be faced. Firstly, there must be a fleet! Secondly, there must be a network of operational centres that can manage the asset fleet. Finally, there must be a bedrock base of cargo owners or forwarders who see sufficient merit in the system to work with DFA to secure ships space. This is all achievable. This is also where the association between DFA and DP World comes into play. DP World, with the largest portfolio of terminal and inland terminal locations in the world, backed by a robust balance sheet, can provide important under-pinning to the DFA’s ambitions to help amend the current system and build more resilience for the next shortage.