Import Maritime Tariffs From China to Mexico 2024 - 2025: DFA Premium Member's Trade Insights

October 23, 2025

5 min read

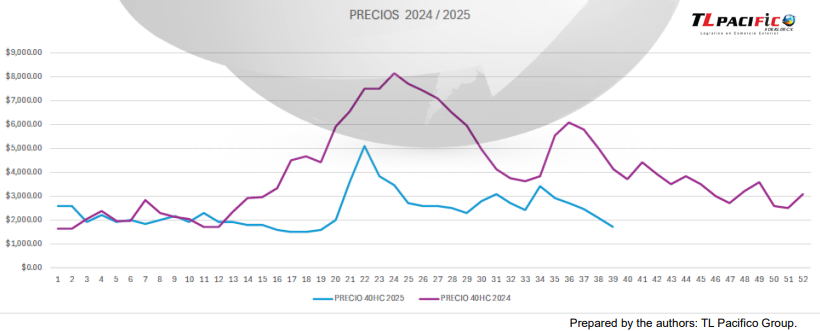

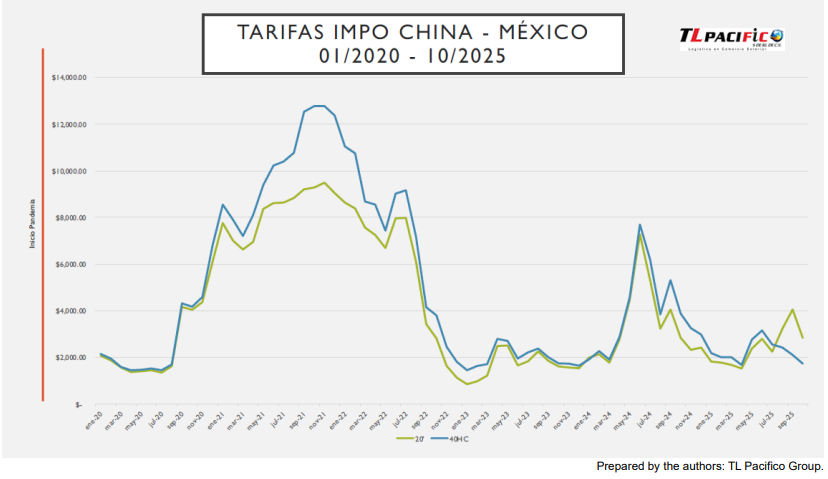

Container shipping has entered a new cycle in 2025, marked by significantly lower rates than in the years of high logistics disruption experienced between 2020 and 2022. What was once a highly profitable market for shipping companies is now facing a complex reality: revenues per TEU transported are below operating costs. This phenomenon is not accidental, but a consequence of multiple structural and circumstantial factors that are reshaping the Global Shipping landscape.

1. ON THE CAPACITY SUPPLY OF THE SHIPS

Another paradoxical inflationary pressure comes from the excess of ships. During the pandemic and the years that followed, major shipping companies took advantage of high revenues to order thousands of new container ships. Now, that fleet is beginning to arrive at the ports, generating a phenomenon of oversupply.

2. THE WORLD'S LEADING SHIPPING COMPANIES HAVE ORDERED NEW SHIPS TO

BE BUILT IN ACCORDANCE WITH SUSTAINABILITY REGULATIONS

• Maersk: You have ordered several vessels capable of operating 100% on green methanol. Part of this fleet is expected to come into operation in the last quarter of 2025.

• MSC: A leader in global capacity, it has increased its fleet with dual-fuel ships (LNG

and traditional bunker), although its focus remains on volume growth.

• CMA CGM: It plans to have more than 120 eco-friendly vessels by 2027, many of them compatible with methanol or LNG.

• COSCO: China's leading shipping company has also been involved in "green" orders, boosted by the Asian country's shipbuilding capacity.

• Hapag-Lloyd: Although more cautious, it has begun to incorporate energy-efficient technology and operates under alliances for more efficient routes.

• All other shipping companies are in the same process.

Currently, container ships under construction worldwide already incorporate sustainable technologies, although key challenges remain: scarce supply infrastructure, high cost of new fuels and the need for specialized technical training to operate these ships.

3. LONGER ROUTES, HIGHER COSTS

One of the main factors behind the tariff hike has been the conflict in the Middle East. Attacks on commercial vessels by Houthi rebels have forced many shipping companies to divert their traditional routes across the Suez Canal to the long and expensive route around the Cape of

Good Hope. This alternative can add between 10 and 15 days to the crossing, with a proportional increase in fuel, operation and transit time costs.

Although it was reported this week that a possible ceasefire agreement between the parties could reopen the passage through the Red Sea, the tariffs have not yet reflected a sustained decline. The impact of such diversions has been so profound that even Maersk's shares fell on news of the potential deal, anticipating a reduction in fares that affect its revenues.

Shipping companies will seek to use more feeder vessels in the distribution of cargo.

4. BLANK SAILINGS: ADJUSTING CAPACITY TO STRENGTH

One of the main indicators of the current imbalance in maritime transport is the increase in blank sailings or cancelled departures. This practice, used by shipping companies to reduce the supply of capacity on routes where demand has fallen, seeks to stabilize rates. However, it also shows the difficulty of filling ships on certain routes, especially Asia-Europe and the Transpacific.

Constant adjustment through scheduled cancellations reduces fleet utilization, increases uncertainty for shippers and reflects the fragility of the market. While it is a useful tool in the short term, its effectiveness diminishes when it becomes the norm rather than the exception.

ADDITIONAL FACTORS

Sustainable Fuels.

Incorporation of new fuels such as: LNG, Methanol, Biomethanol, Ammonia, Nuclear power, etc.

Alternative and low-sulfur fuels, such as VLSFO or green methanol, are significantly more expensive than traditional fuel oil. This has raised the operating costs of shipping companies, especially on long-haul routes.

Example: operating with green methanol can cost up to 2 or 3 times more per ton than conventional fuels, which reduces profit margins.

To meet the requirements of the CII index, many shipping companies are resorting to slow steaming, which:

• Reduces fuel consumption and emissions.

• But it also prolongs transit times, affecting logistics planning.

• It forces itineraries to be readjusted and can cause congestion if there is less

frequency or rotation of ships.

During the years of port congestion and historic rates, shipping companies made heavy investments in new containership construction. By 2025, a large part of these ships are being delivered, generating structural overcapacity in the market.

Today, the global fleet has more space than current demand requires. Although shipping companies have implemented measures such as slow steaming (reducing speed to absorb capacity), the pressure on rates continues. Oversupply, combined with low ship utilization, has created an environment where prices are rapidly eroding.

Added to this is a decline in global demand for goods, derived from political factors such as the increase in tariffs on Chinese products to the United States. This has directly impacted the volumes transported per container, especially on trade routes between Asia, Europe and North America. With less cargo to move, shipping lines compete aggressively to attract customers, often accepting rates below their break-even point. This "price war" harms not only the large lines, but also regional players and smaller operators.

Internal Competition and Alliances in Tension

In a scenario of overcapacity and weak demand, even large shipping alliances have begun to show signs of tension. Although these groups allowed at the time to optimize routes and reduce costs, today strategic differences and the pressure to maintain market share are generating competition among members.

Added to this is the entry of new regional players or independent lines that, with lighter structures, can offer more aggressive rates. All of this intensifies competition and prolongs the downward trend in ocean freight prices.

Digitalization and Operational Efficiency

The digital transformation of the logistics sector has allowed many shipping companies to optimize processes, reduce administrative costs and improve planning. While this has contributed to greater efficiency, it has also raised customer expectations for transparency and price.

The implementation of technologies such as artificial intelligence in fleet management, digital booking platforms and real-time traceability has lowered some barriers to entry for new operators and has pushed traditional shipping companies to reduce prices to stay competitive.

So it is expected that by the end of this year, the trend will be upward from how it is today.

For your inquiries:

Jaime Velez

[email protected]

+523320656450

DFA Premium Member in Mexico